Microsoft just made one of its clearest strategic moves in AI so far.

The headlines are about the models: a first in-house reasoning model, a small coding model, faster transcription, multilingual voice generation, and a stronger image model. Those announcements matter. But I do not think the real story is any single model.

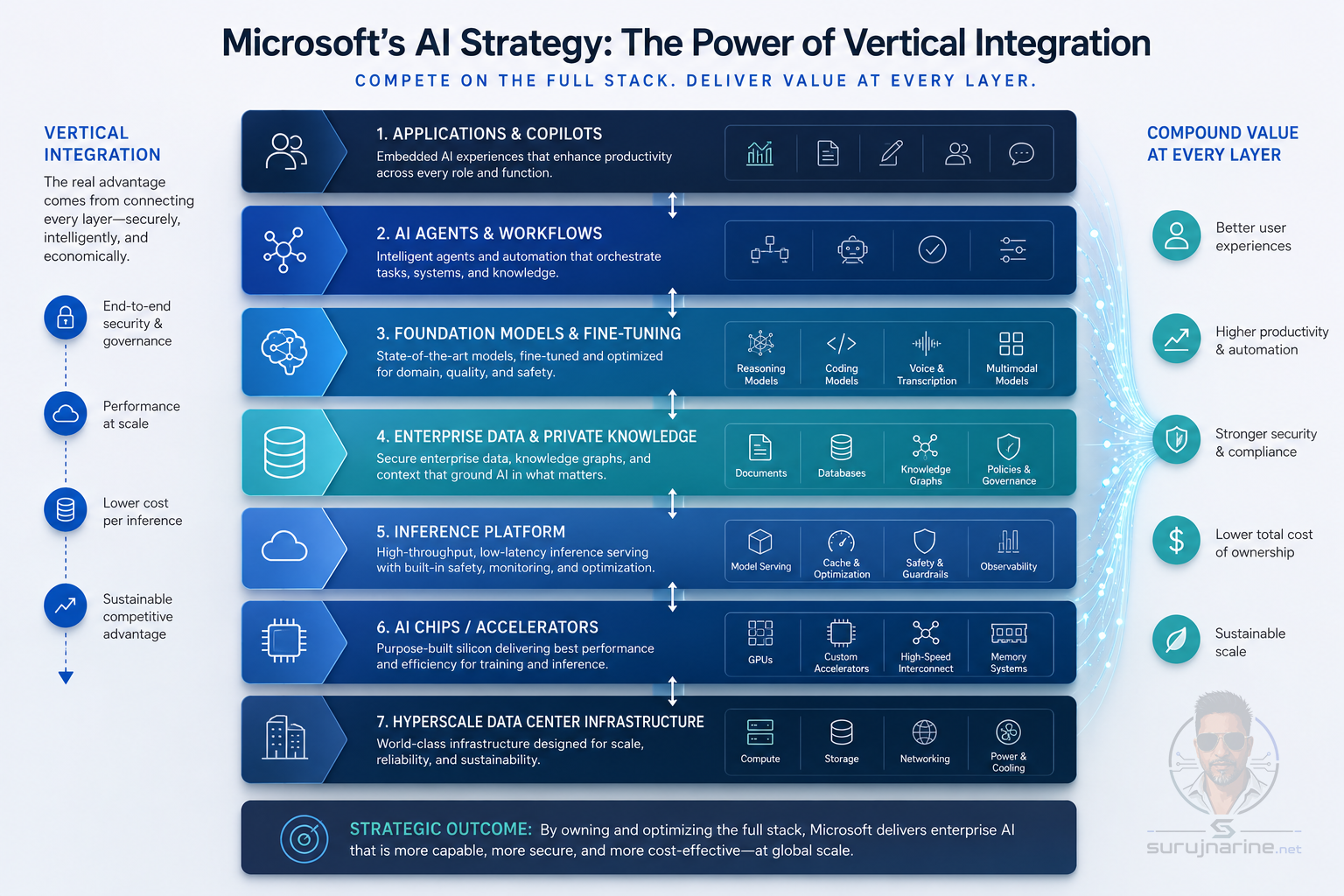

The bigger story is that Microsoft is trying to own more of the AI stack.

Model layer. Enterprise tuning. Inference silicon. Developer distribution. Copilot surfaces. Cloud infrastructure. Governance. Workflow integration.

That is the move.

Because the next phase of AI will not be decided only by who has the biggest frontier model. It will be shaped by who can make AI cheap enough, deployable enough, governable enough, and integrated enough to become part of normal business operations.

Microsoft seems to understand that very well.

This was not seven product announcements

It was a positioning statement.

At Build 2026, Microsoft introduced a new set of in-house MAI models, including MAI-Thinking-1 for reasoning, MAI-Code-1-Flash for coding, MAI-Transcribe-1.5 for speech-to-text, MAI-Voice-2 for multilingual speech generation, and MAI-Image-2.5 for image generation and editing.

On the surface, that looks like Microsoft catching up in several categories at once.

Underneath, it looks more like vertical integration.

The company is signaling that it does not want to depend entirely on rented intelligence forever. It wants to own more of the model layer, own more of the economics of inference, and give enterprises a way to tune AI around their own data and workflows instead of simply consuming generic frontier APIs.

That is a very different strategic posture from having access to someone else's model.

The McKinsey claim is the tell

One of the most interesting parts of Microsoft's announcement was not a benchmark leaderboard. It was the enterprise tuning story.

Microsoft said that after tuning its models for McKinsey's tasks, MAI delivered the highest win rate, outperforming GPT-5.5 on quality while being 10 times lower on cost. It also framed this as part of a broader frontier tuning strategy where enterprise know-how, private data, workflows, and task-specific reinforcement environments become part of the moat.

That is a Microsoft claim, so it should be read with the usual caution.

But if the pattern holds, it is a big deal.

Because it suggests the enterprise AI question may shift from:

Which frontier model is smartest?

to:

Which model-plus-data-plus-workflow system gives me the best quality at the best operating cost for my actual business?

That is a much more practical question.

It is also a much more Microsoft-shaped question.

Microsoft has distribution into the enterprise, existing identity and data footprints, Copilot surfaces, GitHub, Fabric, Azure, and a huge installed base of business workflows. If it can combine good-enough-or-better model quality with materially better inference economics and enterprise tuning, that becomes a very strong position.

This is also a data center story

The AI race is increasingly a data center story.

The romantic version of AI focuses on model breakthroughs. The operational version is about power, cooling, inference efficiency, memory bandwidth, networking, and cost per useful token.

That is where Maia 200 matters.

Microsoft describes Maia 200 as an inference accelerator built on TSMC's 3nm process, with native FP8 and FP4 tensor support, 216GB of HBM3e, 7 TB/s of memory bandwidth, and 272MB of on-chip SRAM. The stated goal is straightforward: improve the economics of token generation.

That is not a side note.

That is Microsoft trying to control the cost structure of AI at the infrastructure layer.

The deeper implication is that AI is pushing the industry away from a world where cloud scale alone was enough and toward a world where cloud providers need differentiated AI infrastructure. The more important inference becomes, the more valuable it is to own the economics of that inference instead of relying entirely on external silicon roadmaps and third-party margins.

That does not mean Nvidia suddenly stops mattering.

Far from it.

It means hyperscalers are increasingly motivated to reduce dependency at the margin, optimize for their own workloads, and build infrastructure that fits their own software and commercial model. Maia 200 is part of that trend.

The next AI battle is economics, not just capability

There is a reason Microsoft keeps talking about efficiency.

As AI moves from demos to enterprise deployment, token cost, latency, throughput, and orchestration overhead start to matter as much as raw capability. A model that is slightly less magical but dramatically cheaper, more governable, and better tuned to the actual task can win a lot of enterprise work.

That has two major implications.

First, enterprises may build around smaller, specialized, tuned systems instead of assuming every use case needs the largest general-purpose model available.

Second, cloud and AI vendors will increasingly compete on the total operating model:

- model quality

- inference economics

- tooling

- fine-tuning workflow

- data integration

- security

- governance

- developer distribution

That is stack competition.

And Microsoft is one of the few companies in a position to play across all of it.

What this means for enterprise AI strategy

For technology leaders, the takeaway is not that Microsoft won.

It is that the enterprise AI market is maturing.

The era of simply plugging into a frontier model and hoping it solves everything is giving way to a more structured phase where several things matter more:

- private data

- workflow fit

- cost efficiency

- model specialization

- infrastructure choices

- governance

In that world, enterprise value may come less from having the absolute smartest raw model and more from building a tuned, cost-effective, auditable AI system around real business work.

That is exactly the kind of terrain where Microsoft tends to be dangerous.

Not because it always invents the category first, but because it understands how to operationalize technology inside large organizations.

A few bigger shifts

Frontier models will matter, but tuned enterprise models may matter more.

The practical enterprise winner may often be the model that is deeply adapted to internal tasks, proprietary data, and operating constraints, not the one that wins the most public demos.

Inference is becoming a first-class battleground.

Training still matters, but inference economics are where enterprise scale gets real. If token generation stays expensive, the business case breaks down.

The AI data center will increasingly be co-designed around AI workloads.

Expect more pressure on power, thermal design, memory architecture, and networking efficiency. The future AI stack is not just smarter software. It is more specialized physical infrastructure.

Distribution still matters.

Microsoft does not need to win only in the abstract model market. It needs to make its AI useful across GitHub, Copilot, Azure, Fabric, Office, and enterprise workflows. That installed base is a strategic advantage.

My takeaway

The most important thing Microsoft just showed is not that it launched several new AI products.

It showed that it wants to be less dependent, more vertically integrated, and more economically competitive across the full AI stack.

That is a serious move.

If the next phase of AI is about getting from impressive capability to scalable enterprise usefulness, then this is exactly the kind of move that matters: own more of the model layer, tune around private enterprise data, control more of the inference economics, and push it all through products enterprises already use.

That has implications far beyond Microsoft.

It means the future of AI will be shaped not only by who has the best model, but by who can turn intelligence into infrastructure, workflows, and sustainable economics at scale.

That is where the next real battle is.

References

Related reading

What Cursor's hypergrowth really teaches us

A case study in timing, workflow ownership, enterprise conversion, and execution speed behind Cursor's rise.

The AWS Outage Is a Reminder That the Cloud Still Has a Physical Layer

Heat, power, and cooling in Northern Virginia — why cloud resilience must be tested against physical reality, not just diagrams and failover plans.